Is your employer-provided life insurance enough?

Plenty of companies offer life insurance as an employee benefit. But those policies may only provide a fraction of the coverage your family will actually need to remain secure financially if the unexpected were to occur. Explore how employer-sponsored life insurance only covers a portion of the overall picture.

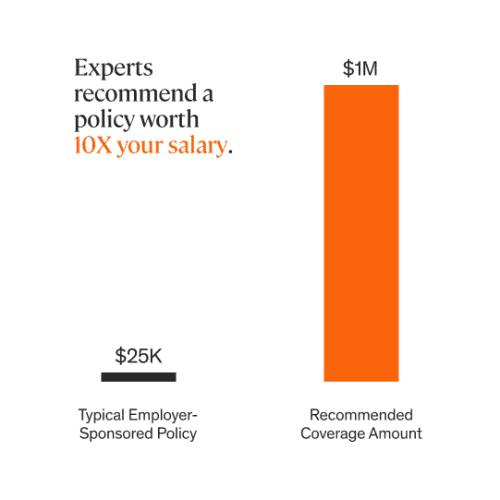

Employer-sponsored life insurance policies typically provide coverage of around 1-2x your annual salary. However, financial experts recommend you carry a minimum of 10x your yearly earnings. If you're relying solely on life insurance through work, your coverage will fall well below what your loved ones need to maintain their current lifestyle.

But the 10x rule is just a starting point. Want a more in-depth analysis of your needs? Try the DIME formula (debt + income + mortgage + education). Total up your outstanding debt, annual income multiplied by the estimated number of years your family needs your income support, your mortgage balance, and the estimated costs of your kids' education.

What happens to life insurance when you leave a job? However you leave your company—job change, layoff, retirement—you may be able to take your employer-sponsored life insurance policy with you. But keep in mind that you'll likely lose the pricing benefits provided by the employer's group rate. That could mean overpaying for insufficient coverage. A smart option is to apply for your own personal life insurance coverage. And, typically, the sooner you apply for individual coverage, the better your rate—and your family's financial future— will be.

/Stocksy_txp316925b6bvV200_Large_2319538_edit_vrxcdc.jpg)

Life insurance typically costs more as you get older or if your health declines. The sooner you apply, the more likely you'll get the coverage you want at a premium that works for your family. All policies offered by Ethos include level term premiums, meaning your price won't increase throughout your policy's term.

Having group term life insurance is a nice perk, but it likely won't cover all your needs. Take pen to paper to determine how much coverage your family really requires. The DIME formula previously mentioned provides a comprehensive picture of your debt, income needs, mortgage expenses, and estimated education costs if you have dependent children. Since your family's life and financial goals evolve, reevaluate your life insurance coverage annually to decide if you have enough or require more.

As long as your life insurance policy remains active, your selected loved ones receive a lump-sum financial death benefit. How they use the cash payment is up to them. The two main types of life insurance are term and whole. Term life is an affordable option where you pay a flat-rate premium for a set period. If you pass away during the specified term, your beneficiaries receive a payment. Whole life covers you for your entire life as long as you pay your premiums with a payout guaranteed upon your death.

Explore the type of insurance that's right for you →

Ethos partners with some of the world's largest and most respected life insurance companies. You get that dependability combined with the convenience of a modern technology company. Our online life insurance application process is quick, easy, and convenient. Once you apply, we'll find the policy and premium customized to your individual needs.