Types of life insurance, explained.

The two main life insurance categories are individual and group. Individual policies are owned by an individual person and within this category, you can choose between permanent (or whole) and term policies. Group life insurance, on the other hand, typically comes in the form of an employer-sponsored life insurance policy you receive as a benefit through work.

/life-insurance-family-on-vacation.jpg)

Permanent versus term life insurance

These are the two main types of individual life insurance you’ll hear about. There are pros and cons to each, but term life insurance tends to be more simple and affordable.

Permanent (whole or universal) life insurance

- This type of coverage can last your whole life and often accumulates cash value that may increase the death benefit, or be accessed early by requesting a policy loan or withdrawal.

- In exchange for the length of coverage and cash value accumulation possibilities, premiums for permanent coverage are typically 10-15X higher than those for term life insurance.

- If the higher premiums are within budget, permanent life insurance can be a good option for those interested in insurance that will accumulate cash value and will not end after a specific term.

Term life insurance

- Term policies last for a specific amount of time (your term), and there is no cash value accumulation. You choose the amount of coverage that would be paid out to your beneficiaries if you die before your term ends. If you die after your term ends, no death benefit is paid. It’s that straightforward.

- Term life insurance premiums tend to cost 10-15X less than permanent life insurance, making it an affordable option for many.

- Term life insurance can be a good option for those who are interested in cost-effective coverage for a specific term, without the higher expenses associated with a cash value policy.

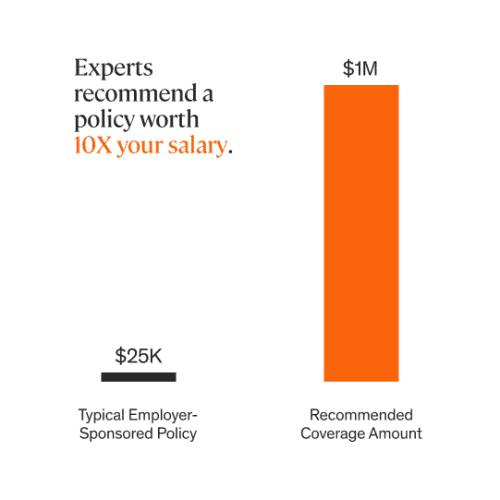

Employer-sponsored (group) life insurance

Group life insurance is where a single contract can provide coverage to a group of people, or its employees. You might already have some life insurance coverage provided to you as an employee benefit. However, this type of policy might only provide a fraction of the coverage you need. For this reason, many people buy an individual term life insurance policy to supplement the coverage they receive through work.

Please note that all prices quoted are subject to change, including due to underwriting.